EPISODE #746 AAG cuts workforce- Finance of America to close forward division

A rapidly-changing market has led two of our industry’s largest lenders to make big changes. One reduces its reverse mortgage workforce, another will close its traditional/forward division and focus on its productive reverse mortgage channel.

Other Stories:

Finance of America Mortgage closes forward unit- reverse remains the focus

Epigrams- they were engraved on statues, the walls of homes in Pompei, and even on the rock of the Temple of Apollo. Think of them as the ancient predecessor of today’s memes. An epigram is a pithy saying often packed with wisdom or humor – it’s often written in verse. Just as many on social media find memes irresistible, epigrams still carry weight in the twenty-first century. As the famous poet and playwright Oscar Wilde puts it, “I can resist everything but temptation”. So let’s indulge our appetite for some famous, insightful, and irreverent epigrams.

“An economist’s guess is liable to be as good as anybody else’s” – Will Rogers

“The best revenge is not to be like that.” -Marcus Aurelius

“Character is fate.”- Heraclitus

“Action expresses priorities.” -Mohandas Gandhi

“If you can’t be a good example, you’ll just have to be a horrible warning” – Catherine the Great

“This is not your responsibility, but it is your problem.” – Cheryl Strayed

“You never know who’s swimming naked until the tide goes out.” – Warren Buffett

“Live as if you were living a second time, and as though you had acted wrongly the first time.” – Viktor Frankl

“Justice delayed is justice denied” – Unknown

“Expectation is the root of all heartache.” – William Shakespeare

“Be curious, not judgmental.” – Walt Whitman

“Education isn’t something you can finish.” – Isaac Asimov

“We are all broken- that’s how the light gets in.” – Ernest Hemingway

“You may have to fight a battle more than once to win it.” – Margaret Thatcher

“And now that you don’t have to be perfect, you can be good.” -John Steinbeck

California: The lynchpin of the HECM’s economic outlook

Since 2009 California has led all states for total HECM endorsements. In fact, according to the Fiscal Year, 2021 Independent Actuarial Review of the Mutual Mortgage Insurance Fund, California accounted for 26% of all HECM endorsements in the fiscal year 2021. Florida, Arizona, Colorado, and Texas trail significantly in endorsements accounting for 7-8% of overall loan volume respectively. California is home to some of the nation’s highest-valued homes and also has seen some of the most rapid growth in Home Price Appreciation. Consequently, any broad declines in home values in the Golden State will have a marked impact on the 2023 and 2024 economic valuation of the HECM Program.

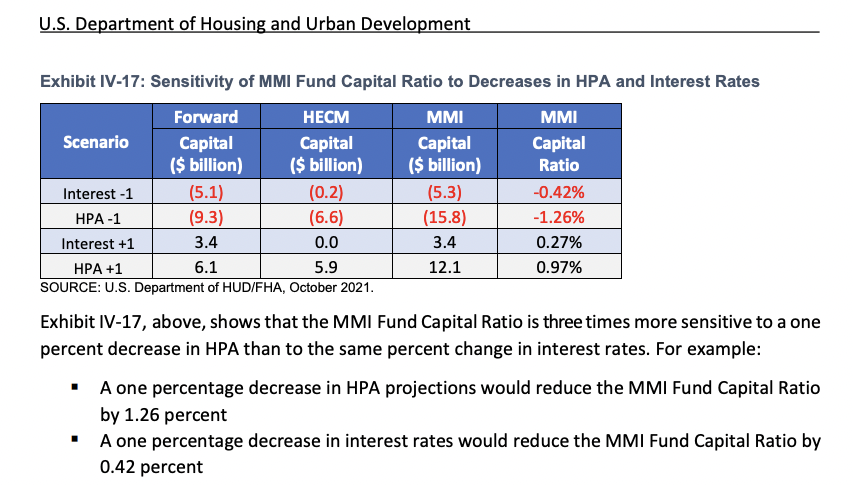

FHA acknowledges this sensitivity in its 2021 report. “HPA is a lagging indicator that tends to overstate [read more]

the health of the economy during good times and the weakness of the economy during bad times. Because the MMI Fund Capital Ratio is so closely tied to HPA, the assessment of FHA’s financial health represented by the ratio can change materially and quickly with changes in both actual and projected home values.” The operative word is overstated. To further illustrate this point the Mutual Mortgage Insurance Fund’s capital ratio is three times more sensitive to a one percent drop in home price appreciation than a one percent decrease in interest rates.

All of which begs the question, where does the California home market stand today? After a decade of generally consistent gains, home values have turned negative. Zillow reports that home price in Southern California is now 6% below the all-time high reached in May.

For a closer examination, we’ll go to Fortune’s interactive map which shows the markets most likely to see a drop in home prices in the coming year.Markets in dark red are very likely to see home price reductions, those in light pink are rated high, purple is medium, and light blue are the markets less likely to see home price drops. Now moving over to Shasta County California and Redding the county seat, I can see my hometown is very likely to see price drops which I can confirm first hand having seen dozens of listings drop their asking price and closings coming in 10-17% lower. However, we’re not alone with most of the southern California markets also showing a high probability of a fall in home values. Many of these at-risk markets have already seen significant erosion in home values. Between May 2022 and August Shasta county saw values fall by -2.78%, Sacramento values fell by -6.03%,

San Francisco values dropped by -7.8%, and San Jose fell over 10.5%! Los Angeles, Riverside and San Diego also saw values fall.

Looking at metros in other states we can see some of the previous hottest markets poised for a fall. For example, Boise Idaho. The median sales price of single-family homes in the greater Boise area has fallen from a high of $550,000 in May to $510,000-a drop of 8 percent. In the same time period, Reno sale prices also dropped 8% from $625,000 to $580,000. Austin Texas appears to be in a free fall collapsing from a median sales price of $720,000 in May and plummeting to $620,000- a drop of 14% in just three months! If that pace continued Austin prices would fall by 56% year-to-year. It should be noted that two forces have not been factored into this forecast which may accelerate the fall of home values; a recession and continued inflation increasing foreclosure filings.

In conclusion, we’ve been on this journey before; at least those of us who were originating prior to the 2008 housing crash. Whether it’s a coming housing crash or correction our willingness to look at market signals and acknowledge their likely outcome only serves to help us prepare for the future and adjust our mindset and business strategy to succeed. How do you expect California home values will impact reverse mortgage lending? Let us know in the comment section below.

Are we headed for a major market crash? Are there things to consider like reverse mortgages to help weather eroding market conditions? Several experts weigh in with their advice…

Like a passenger on the Titanic discovering the dining table they ate on the evening before is now their life raft, many older homeowners may discover their home was their saving grace all along

The Consumer Financial Protection Bureau (Bureau or CFPB) is seeking comment from the public about (1) ways to facilitate mortgage refinances for consumers who would benefit from refinancing, especially consumers with smaller loan balances; and (2) ways to reduce risks for consumers who experience disruptions in their financial situation that could interfere with their ability to remain current on their mortgage payments. The press release refers to this solicitation as a Request for Information (RFI).

Other Stories:

Don’t Be Complacent During The “Critical Retirement Decision” Zone

Hurricane Ian traumatized Floridians. It also erased their nest egg