Older Americans will soon face a financial day of reckoning. Here’s why…

Continue reading

Older Americans will soon face a financial day of reckoning. Here’s why…

Continue reading

Three factors will shape 2023 reverse mortgage production…

Continue reading

4 ways to keep from sinking in today’s ugly market

Continue reading

Retirees tap into the value of their accumulated assets such as 401(k)s, IRAs, etc but rarely do they consider the sacred cow of tapping into their home’s equity.

Continue reading

Future access to a HELOC is NOT guaranteed. What about a HECM?

Continue reading

The 2023 HECM Limit is likely to exceed $1 million! Here’s why…

Continue reading

“The Fed will push until something breaks”. That’s been a popular line among economists and analysts according to a recent column in Fortune

Continue reading

Since 2009 California has led all states for total HECM endorsements. In fact, according to the Fiscal Year, 2021 Independent Actuarial Review of the Mutual Mortgage Insurance Fund, California accounted for 26% of all HECM endorsements in the fiscal year 2021. Florida, Arizona, Colorado, and Texas trail significantly in endorsements accounting for 7-8% of overall loan volume respectively. California is home to some of the nation’s highest-valued homes and also has seen some of the most rapid growth in Home Price Appreciation. Consequently, any broad declines in home values in the Golden State will have a marked impact on the 2023 and 2024 economic valuation of the HECM Program.

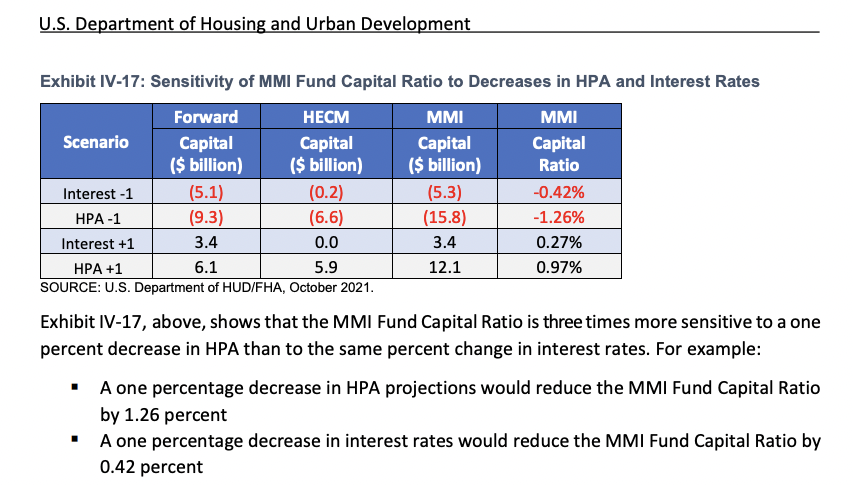

FHA acknowledges this sensitivity in its 2021 report. “HPA is a lagging indicator that tends to overstate

[read more]

the health of the economy during good times and the weakness of the economy during bad times. Because the MMI Fund Capital Ratio is so closely tied to HPA, the assessment of FHA’s financial health represented by the ratio can change materially and quickly with changes in both actual and projected home values.” The operative word is overstated. To further illustrate this point the Mutual Mortgage Insurance Fund’s capital ratio is three times more sensitive to a one percent drop in home price appreciation than a one percent decrease in interest rates.

the health of the economy during good times and the weakness of the economy during bad times. Because the MMI Fund Capital Ratio is so closely tied to HPA, the assessment of FHA’s financial health represented by the ratio can change materially and quickly with changes in both actual and projected home values.” The operative word is overstated. To further illustrate this point the Mutual Mortgage Insurance Fund’s capital ratio is three times more sensitive to a one percent drop in home price appreciation than a one percent decrease in interest rates.

All of which begs the question, where does the California home market stand today? After a decade of generally consistent gains, home values have turned negative. Zillow reports that home price in Southern California is now 6% below the all-time high reached in May.

For a closer examination, we’ll go to Fortune’s interactive map which shows the markets most likely to see a drop in home prices in the coming year. Markets in dark red are very likely to see home price reductions, those in light pink are rated high, purple is medium, and light blue are the markets less likely to see home price drops. Now moving over to Shasta County California and Redding the county seat, I can see my hometown is very likely to see price drops which I can confirm first hand having seen dozens of listings drop their asking price and closings coming in 10-17% lower. However, we’re not alone with most of the southern California markets also showing a high probability of a fall in home values. Many of these at-risk markets have already seen significant erosion in home values. Between May 2022 and August Shasta county saw values fall by -2.78%, Sacramento values fell by -6.03%,

San Francisco values dropped by -7.8%, and San Jose fell over 10.5%! Los Angeles, Riverside and San Diego also saw values fall.

Looking at metros in other states we can see some of the previous hottest markets poised for a fall. For example, Boise Idaho. The median sales price of single-family homes in the greater Boise area has fallen from a high of $550,000 in May to $510,000-a drop of 8 percent. In the same time period, Reno sale prices also dropped 8% from $625,000 to $580,000. Austin Texas appears to be in a free fall collapsing from a median sales price of $720,000 in May and plummeting to $620,000- a drop of 14% in just three months! If that pace continued Austin prices would fall by 56% year-to-year. It should be noted that two forces have not been factored into this forecast which may accelerate the fall of home values; a recession and continued inflation increasing foreclosure filings.

In conclusion, we’ve been on this journey before; at least those of us who were originating prior to the 2008 housing crash. Whether it’s a coming housing crash or correction our willingness to look at market signals and acknowledge their likely outcome only serves to help us prepare for the future and adjust our mindset and business strategy to succeed. How do you expect California home values will impact reverse mortgage lending? Let us know in the comment section below.

Redfin Monthly Housing Market Data (Charts shown in video)

2021 FHA Annual Report to Congress

Odds of falling home prices in your local housing market, as told by one interactive map

Rising mortgage rates are sending home prices lower

[/read]

Part 2 of our exclusive interview with Dan Hultquist examines the impacts of public perception, policy, and property values on the HECM program.

Continue reading

Dan Hultquist shares the 6 Ps that impact the overall health of the reverse mortgage industry…Part 1/2

Continue reading