EPISODE #681 HECM Refis are not growing our market

RMI’s John Lunde told RMD while HECM endorsements are strong our industry’s production is not quite as robust as one may believe when considering HECM-to-HECM refinances.

Other Stories:

Will there be a wave or a trickle of evictions?

Homeowners are hurting but property tax panel looks elsewhere

As moratoriums end, seniors stand to lose the most

A federal ban on evictions expired Saturday, July 31st. Consequently millions of Americans are facing the specter of housing insecurity or homelessness.The financial protections put in place for millions of households throughout the pandemic including foreclosure moratoriums, stimulus checks, and unemployment benefit bonuses only delayed the inevitable for some.

While the federal government has extended eviction and foreclosure protections multiple times, it’s unlikely we will see another intervention. However, as we are recording today’s show we should note that anything can happen. Case in point- the rapid increase of new cases of the Covid Delta Variant led the CDC to reverse its recent mask guidance for vaccinated individuals. While Covid hospitalizations and deaths had dropped precipitously the government could justify further stimulus and housing protections due to the potential economic impact of the Delta variant strain.

While eviction moratoriums are scheduled to end on July 31st struggling homeowners have until…

[read more]

September 30th to request a mortgage forbearance. Homeowners who obtained a forbearance last spring have up to 18 months of protection. That means someone who entered forbearance last March would exit forbearance this month. Their choices would be to obtain a loan modification, sell the home, or let the mortgage go into default. Those with an FHA, USDA, or VA loan are not required to make a lump sum repayment of missed payments.

The good news is only 2.9% of all active mortgages are over 90 days late reports the Wall Street Journal. That’s a marked improvement from the 4.4% of households who were delinquent last summer. The bad news is roughly 1.55 million are still seriously delinquent and some of those are over the age of 60. Those who stand the lose the most are those who’ve paid down their mortgage balance significantly over the years and have a strong equity position in the property which would be lost in a foreclosure.

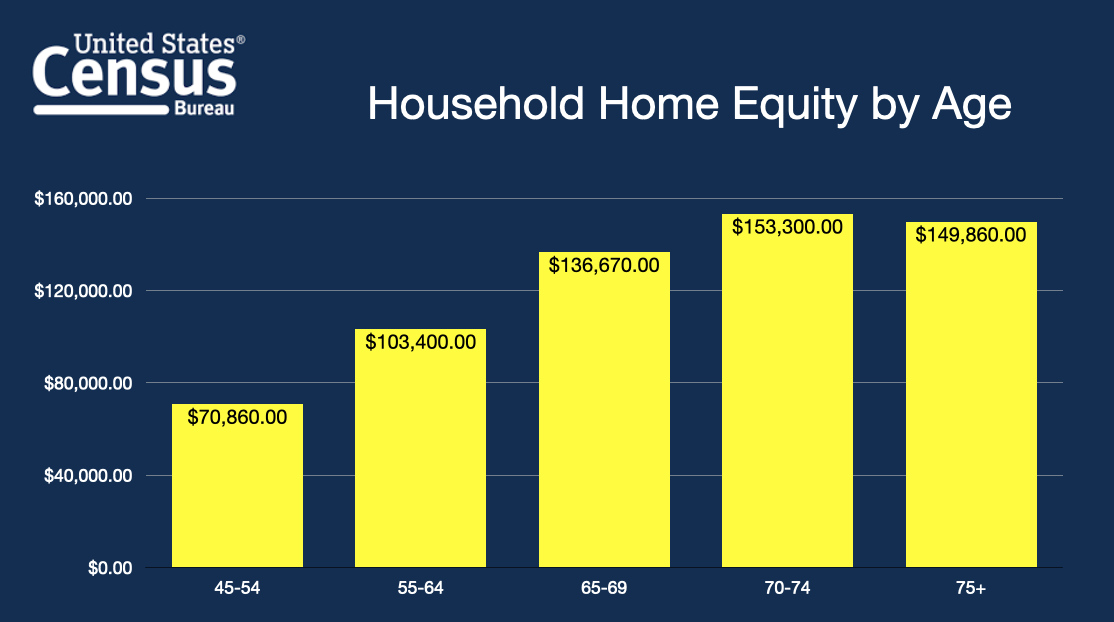

Of all age groups, older homeowners stand to lose the most having accrued significant equity. Census Bureau data shows households aged 45-54 have an average of $70,860 in equity totaling 64% of their net worth. Those aged 55-64 have $103,400 in equity for 61% of their net worth. Homeowners between 70 and 74 have $153,300 in home equity totaling 72% of their net worth. That spells trouble for the struggling homeowner who is delinquent on their mortgage and the opportunity for many to escape potential eviction with a reverse mortgage. This data also confirms that the banks stand to profit the most by foreclosing on older homeowners with substantial equity.

All things considered, we can conclude the following outcomes are likely- There will be a spike in foreclosures across the country, how big we don’t know. Those foreclosures will impact housing values and stand to improve existing home inventory.We can also expect further government intervention and stimulus, especially considering the strong reactions to the Delta variant despite vaccinations. Those emergency measures when added to previous protections will come at a significant economic cost- one that older American’s are ill-suited to absorb.

Moratoriums are winding down and struggling older Americans stand most at risk of losing their accumulated home equity. That’s where you, our viewers, as reverse mortgage professionals can offer a potential remedy to restore housing and financial security.

A reset is coming to the U.S. housing market and reverse mortgage lending

A return to the ‘New Normal’

A day of reckoning is coming. It’s not doom and gloom. It’s an economic reality. Think of it as the natural end result when a series of mistakes and irrational decisions must be paid. After an unparalleled run the economy and the housing market always seek equilibrium. Now how that exactly plays out we don’t know. But what we can be certain of is there will be an adjustment.

The surge in housing prices has provided an umbrella for many. Extra cash for those who’ve taken a cash-out refinance. A line of credit for homeowners who’ve secured a home equity line of credit. Or a first-time reverse mortgage for older homeowners who are looking to take advantage of today’s ideal market conditions. Then, of course, there are the 4 out of 10 reverse mortgage applicants who are refinancing their existing HECM loan into another to harvest more of their home’s value, and perhaps secure a lower starting interest rate.

Each have benefited although not equally.

[read more]

Borrowers who’ve taken out a HELOC should recall the words of Mark Twain. “A banker is a fellow who lends you his umbrella when the sun is shining, but wants it back the minute it begins to rain.” That rain is when home values drop and the umbrella is the open line of credit HELOC lenders will reduce or freeze altogether.

But there’s another day of reckoning. One which motivates sage mortgage professionals to play the long game. A view that looks beyond today’s hyperactive market and plans for a return to moderate home appreciation and realistic interest rates.

One person who’s taken the long view when it comes to our industry’s market is John Lunde- founder and CEO of Reverse Market Insight. “Given the preponderance of H2H refi activity we’ve been seeing, it looks to me as though the industry could be testing the limits of loans available to be refinanced in some of the historically higher volume areas,” Lunde said in a recent Reverse Mortgage Daily column. Another concern is the leading indicator of future endorsements – FHA case number assignments for new HECM applications. After steady application volume increases last spring and fall case numbers fell in the winter months to rebound to a high of 7,564 case number assignments this March. Following that high-water mark submitted applications fell 13% in April and and 9% in May.

The tapering of application volume may be the result of the HECM-to-HECM refinance boom simply running out of fuel. “Interest rates for new production HECMs are at or near the minimum expected rate, so refinance burnout should start to occur, all else equal,” New View Advisors partner Michael McCully tells RMD. “The industry will need to stay alert on appraisal quality as the impact of lower rates producing genuine net tangible benefit to borrowers recedes.”

The proverbial ‘day of reckoning’ is as natural as the ocean’s tides. The trick is to know when the tide is receding and have a plan in place to continue catching new business as the waters recede. That day may come well before the Fed hikes interest rates so the question is how do each of us prepare to succeed in a new market?

EPISODE #680 Data shows advisers in Australia reluctant to discuss equity release strategies

“New research has found that financial advisers are not considering the government’s Pension Loan Scheme (PLS) when developing strategies for retirees.”

Other Stories:

Reverse Market Insights ‘Market Minute’

MarketWatch: Should seniors get a reverse mortgage?

EPISODE #679 The HECM is Improved- Issues Remain says FHA

FHA’s deputy assistant secretary for single-family housing says while the financial position of the federally-insured reverse mortgage has improved, areas of concern remain.

–

Other Stories:

Survey says it’s a bad time to buy a home spouse

The Fed will keep the punch bowl full- Markets surge

“I lost my job during the pandemic. Now I have $40,000 in credit card debt”. Similar tales of economic devastation as a result of the Covid-19 pandemic are not limited to younger working Americans. In fact, many older workers who were preparing for retirement now find themselves saddled with much more debt than they had one year ago. Some tapped into their retirement savings without penalty thanks to special emergency provisions of the coronavirus CARES Act.The true impact of the pandemic on those approaching retirement remains to be seen. [read more]

Unemployment checks and stimulus payments only went so far in mitigating a job loss, a reduction of hours, or the increased cost of living as inflation continues to surge. As a result many may consider postponing retirement or working a side-hustle to bring in a bit of extra income each month. The Wall Street Journal reports, “The Labor Department reported Tuesday that its consumer-price index increased 5.4% in June from a year earlier. Excluding volatile food and energy categories, prices rose 4.5% from a year earlier, the most in 30 years.” Older homeowners feeling the squeeze of inflation or cut in income have several choices. Cut expenses, work longer, get a part-time job, start taking Social Security benefits earlier or later, or perhaps looking to their home’s value.

Options are your best asset when facing a financial challenge. While every older homeowner may not need to seriously consider getting a reverse mortgage, millions should but never do either from a sheer lack of awareness or fear having been told by friends or the media to avoid the loan altogether. Such prejudices preemptively eliminate a strategy when practical solutions are needed most. With this in mind we should discuss what options the homeowner has considered so far and why they have not chosen them.

Here are several alternatives to a reverse mortgage that may be considered and their benefits and liabilities.

First, refinancing into a lower interest rate. While this may lower the monthly principal and interest payment a couple hundred dollars each month- many are restarting their amortization and in effect will be saddled with required payments for decades.

Then there’s the cash-out refi. While this certainly borrowing at a low interest rate the homeowner’s monthly payments may actually increase with a higher starting principal loan balance.

Others may contemplate selling and downsizing to reduce monthly expenses but few do preferring to stay put . Getting a HELOC or home equity line of credit sounds appealing but there’s still a required monthly payment and payments will increase after the initial draw period expires.

Most of the so-called alternatives to reverse mortgages presented in the press are short-term solutions for a long term problem. In other words, they focus on the immediate need often ignoring the enduring need to meet their monthly cash flow challenges.

All things considered, despite short-term unemployment bonuses, mortgage forbearance, and stimulus checks millions of older Americans are in need of a long-term solution and strategy that helps meet their needs for decades to come- not one that gives them a cash infusion and new debt that further strains their cash flow. [/read]

EPISODE #678 Forbes: The pandemic exacerbated the retirement savings gap

“We still do not know all the long-term consequences for the economy in general and retirement savings in particular. There are some early indicators worth considering…”

Other Stories:

National Mortgage News: The Florida Supreme Court says lender can foreclose on non-borrowing spouse

Fox Business: Housing market showing signs of cooling