“She was feeling panicky and angry. Her 80-year-old mother, Rhonda, had just bought another new car she could not afford. Briana explained that her mother’s funds were limited, but she kept insisting on living the life she had before her husband passed…”

Other Stories:

Find income first to insure against retirement risks

While economic stimulus measures stopped further economic damage in the early days of the pandemic it certainly comes at a cost. That cost is inflation should there be too many dollars chasing American goods and services. However, almost as if defying economic gravity U.S. inflation remains below its two-percent target. Certainly, there was a noticeable spike in food prices early this spring…

Are we seeing the early signs of another mortgage crisis or housing bubble?

Perhaps you’ve noticed that housing prices are blowing up despite an uncertain economy and what appears to be a building second wave of COVID-19 infections. At this point, most of us are ready to accept some good news. However, there are some indicators that we are approaching a housing crisis while certainly, we have solid market indicators of improvement. As one Polish poet put it, “the truth usually is in the middle. Most often without a tombstone. Let’s dive in.

First, we will see a spike in evictions- not because landlords are booting out non-paying tenants, but because those property owners cannot pay the mortgage to the bank when they are no longer receiving rent payments. While this does not directly impact senior homeowners it will contribute toward increasing housing inventory which has a direct impact on housing prices. Next, let’s look at the state of the market comparing Black Knight’s July and August Mortgage Monitor reports.

[read more]

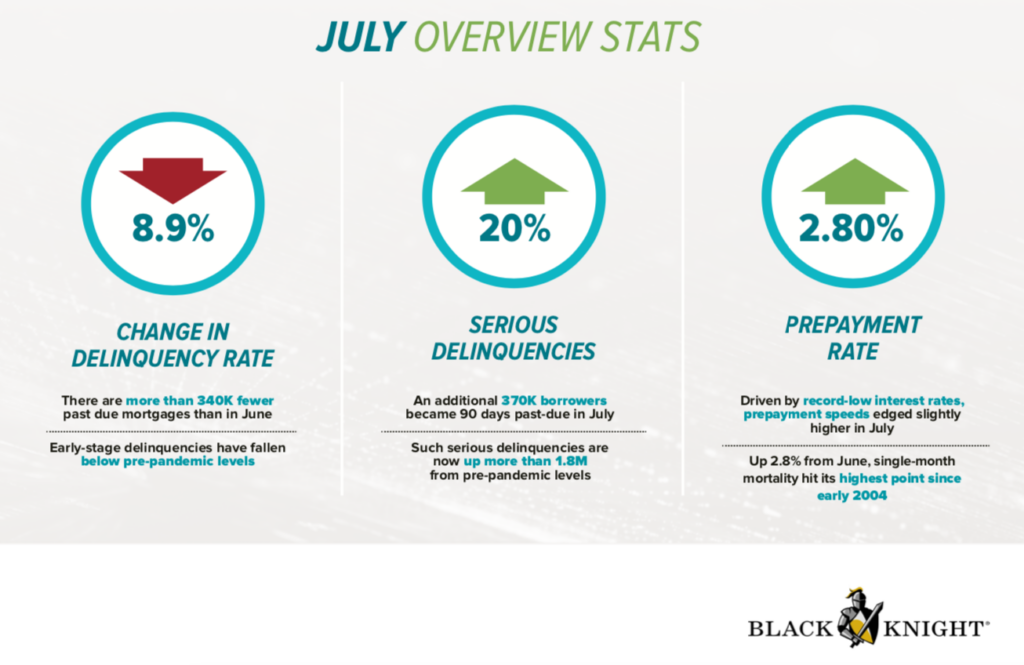

In its July report Black Knight’s stats who show serious mortgage delinquencies- that’s those who are 90 days past due or longer- jumped 20 percent in July for a total of 1.8 million more delinquencies before the pandemic. However, the overall delinquency rate fell by nearly 9%.

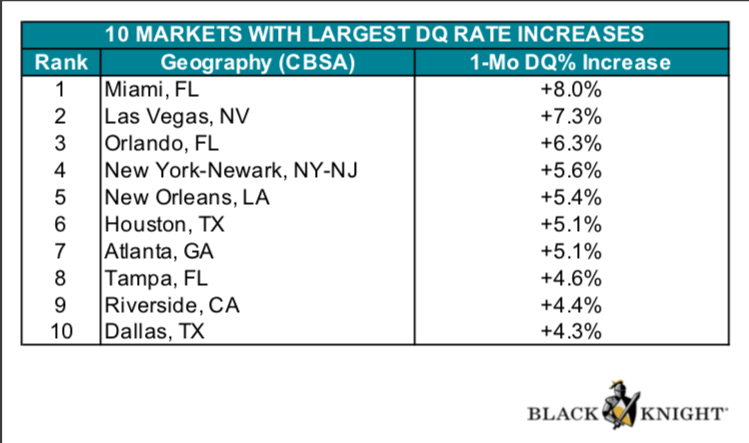

Now, this is where our viewers serving some of our nation’s largest metros will want to pay attention. Here are the ten cities that had the largest increase in delinquencies in July. Florida holds three spots with Miami, Tampa, and Orlando. It’s not surprising to see New York and New Jersey on the list as two of the areas hardest-hit by COVID-19. Cities with the highest delinquencies will see more future foreclosures which naturally increases inventory and lowers prices. The markets with the largest delinquency increases are most likely those where state or local officials have enacted strict shut-down measures shuttering small businesses and spiking unemployment rates. However, keep in mind if we do see a reset in home values it historically has begun in larger metros and then trickles down to smaller communities.

Now on to some positive signs of improvement. The rate of serious delinquencies slowed from July’s 20 percent to only 5 percent growth in August. As the U.S. GDP jumped nearly 33% in the third quarter this year and unemployment rates continue to drop many hope that requests for forbearance plans continue to dwindle after their spike earlier this spring. Outside of historically-low interest rates, the continued lack of housing inventory is sustaining current housing prices. Mortgage delinquencies 100-113% higher than last year as millions found themselves unable to earn an income while sheltering in place, The good news is that many of these individuals are going back to work as evidenced by 41% of those were in a COVID-19 forbearance plan have resumed making their monthly payment.

While these are positive signs of a partial recovery uncertainty remains our biggest challenge. Black Knight Data & Analytics President Ben Graboske explained, “At the current rate of improvement, delinquencies would remain above pre-pandemic levels until March 2022. What’s more, when the first wave of COVID-19-related forbearance plans reach their 12-month expiration period, we would still have a million excess delinquencies.”

In conclusion, what we have is a mixed bag. What could be a looming housing crisis, positive economic indicators, millions resuming their mortgage payments, and of course a red-hot housing market? Our best approach is a stoic one- don’t overindulge in dire predictions, watch key market indicators closely, and consider adjusting your marketing efforts outside larger metros should housing trends turn sour in urban markets.

Resources mentioned in this episode:

BLACK KNIGHT’S JULY 2020 MORTGAGE MONITOR [READ]

BLACK KNIGHT’S AUGUST 2020 MORTGAGE MONITOR [READ]

Mortgage forbearances are being extended. How will home values and borrowers be impacted once they end?

It’s compassionate and pragmatic. Mortgage forbearance allows borrowers to suspend or reduce their monthly payments, however, delinquent payments must be repaid. The good news is homeowners with a federally or GSE-backed mortgage (FHA, VA, USDA, Fannie & Freddie) are protected from a lender initiating foreclosure until December 31st of this year thanks to the CARES Act. FHA-insured Home Equity Conversion Mortgage borrowers are protected under this provision.

[read more]

However, there is a less-publicized provision of the Coronavirus Aid Relief & Economic Safety act; a provision that is certain to have a major impact on the housing market and home values.That provision is the right for the aforementioned homeowners to apply for up to six months and if desired another extension for up to 360 days. No documentation of financial hardship is required to qualify. Basically, that means millions of American homeowners will not be making a payment for up to one year. In essence, our government has attempted to stem a tidal wave of foreclosures and slow damage to our fragile economy delaying the inevitable. The silver lining is home values should remain relatively stable during this temporary calm. That’s a win for reverse mortgage originators who can offer more borrowing power with high home values and low interest rates. Home sales slowed to a crawl in this spring as the first waves of COVID-19 hit our shores. Then the summer months brought record-breaking home sales volumes

as a flood of pent up demand hit the market.

But what happens after mortgage forbearances work their way through the system? Some housing analysts predict 1.9 million or 40% of those in forbearance will end up defaulting. That’s a sobering number but nowhere close to the 3.1 million foreclosure filings seen in the 2008 housing crisis which created a glut of housing inventory driving prices down. A correction in housing values is assured in a cyclical real market but it’s unlikely we’ll see home values plummet immediately. The hope is the air will be released slowly from the housing bubble we find ourselves in today. However, eventually, a toll will be extracted from the housing market for the unprecedented shutdown of our national economy.

Housing prices are marching to the beat of a different drum and seniors are part of the new rhythm which is further constraining housing inventory. “Seniors are scaling down at a far slower rate than in the previous, additional constraining supply. “We were predicting that baby boomers, like past generations at their age, would move into apartments, condos, or to their second homes en masse,” says Ed Pinto- Director of the American Enterprise Institute in a recent Fortune Magazine column. “That isn’t occurring. The main reason they aren’t moving is that their adult children move back in and work from the home they grew up in.”

Two things will mitigate and deflation in housing prices. Housing demand and employment. As more Americans regain employment they are more likely to voluntarily decline further mortgage forbearance and resume making payments. All things considered, a gradual deflation is preferable to a sudden bursting of a housing bubble.

Taking their winnings off the table:

Are seniors over-invested in their home?

Let’s say in January 80% of your assets were invested in hotel and entertainment stocks that made you a healthy chunk of change. For sake of argument, let’s say these stocks consistently out-performed your expectations. Then came March and the arrival of the novel coronavirus. If you found yourself holding these positions after the pandemic broke you probably got clobbered in the market.

Much like being over-invested in one or two companies, many are over-invested in their home. That’s a point Hometap Equity Partners CEO & Cofounder Jeffrey Glass made in a last month’s RMD virtual event HEQ- the future of home equity in retirement. If the bulk of a client’s wealth was tied up in one stock a financial professional is likely to strongly recommend diversification. “If that were a stock, and you had 60-90% of your net worth tied up in one stock, no matter how much you love that stock, any financial advisor would tell you you’re over-concentrated, particularly since you’re over-concentrated in an asset that’s illiquid,” While Glass’ was speaking in the context of alternate equity products, his analogy nevertheless rings true.

So what about housing wealth?

[read more]

To be frank, home equity is an illusion that exists on paper until it is separated from the home. You can almost still hear the echoes of excited voices twelve years ago boasting of their newfound ‘wealth’ or equity they ‘made’. We all remember how that story ends.

The point is the equity, or value if you prefer’ in the bricks and mortar of a home is neither safe nor guaranteed to be there tomorrow. That leaves older homeowners with two choices to extract equity: sell and ‘right-size’ into a new home at today’s prices or separate a portion of the home’s value and remain in place. The former requires one to uproot themselves and later a tool to extract cash from the roof over their heads. So let’s stop here, right now for just a moment and ask ourselves this question. Will home values continue to rise in 2021? To be honest, we don’t know. There may be indicators of a correction but perhaps we should recall the lyric’s from Blood Sweat & Tears hit ‘Spinning Wheel’ ..” What goes up must come down. Spinning wheel got to go ‘round”. And go ‘round does the housing market go. It’s a cyclical market that ebbs and flows. Many experts see employment as the lynchpin of future real estate values.

All of which leads us to our original question. Should older homeowners be taking some of their winnings or equity off the table? Perhaps. The two hurdles that must be cleared are the fear and misunderstanding surrounding reverse mortgages, and the upfront costs to diversify their ‘equity holdings’.Before diving into the intricacies of how a HECM works it’s best, to begin with, the broad brush strokes. “Do you plan on living in your home for the foreseeable future?” And the bonus question, “Do you believe home values will continue to go up in the next year or two or go down?”. Even if they’re not reading the Wall Street Journal each week most homeowners are generally aware of the real estate market’s performance and more importantly, they’re old enough to remember earlier housing downturns.

So what are their options? You know them well. Besides selling there’s the favorite recommendation of media ‘experts’- a HELOC. Great, but now they’ve got a monthly payment in addition to their existing mortgage if they have one. Sell? The fact is most prefer to age in place? That leaves us with the question- how would you leverage your home’s values, take some of the risks of a fall in home values off the table, and not be saddled with a payment? Correct me if I’m wrong, but that seems to point in one direction- a reverse mortgage. Even more so a Home Equity Conversion Mortgage with a line of credit.

Equity makes great conversation over coffee but it’s meaningless and most importantly vulnerable until it’s separated from the home.

Four ways to shore up the HECM BEFORE removing it from FHA’s Mutual Mortgage Insurance Fund

For nearly four years there have been repeated calls to remove the Home Equity Conversion Mortgage program. The HECM was placed into FHA’s insurance fund which backs both traditional and reverse loans in 2009. As HECMs originated at record-high values prior to the housing crash terminated or were placed into assignment many began to ask if the program should no longer be commingled with the larger fund. Last year the Trump Administration’s housing finance reform plan echoed this concern. 4 years earlier an Urban Institute study called to remove the HECM citing the program’s volatility in calculating the program’s valuation each year.The report states “If we assume that half the HECM business is at a fixed rate and that each 1 percent rise or fall in rates causes a 12 percent fall or rise in the value of the loan, that would explain most of the drop in the value of the fund last year and much of the rise in the value of the HECM book of business this year”. With interest rates falling significantly in late 2019 and in 2020 we should expect an improved economic valuation of the HECM.

However, if Congress ultimately approves the move the following issues should first be addressed.

[read more]

Improved accounting

Some have argued that Congress has not fully funded the technology needs of an agency that supervises billions of dollars in domestic loans backed by the federal government. FHA’s 2017 Annual Management Report noted the challenge stating, “The loan origination systems of FHA’s Single Family business have an average age of more than 18 years, with the Computerized Homes Underwriting Management System (CHUMS) exceeding 40 years. Similarly, the systems supporting the servicing, default, claims and REO areas have an average age of 14 years.” However the report added, “FHA management considers the existing systems capable of sustaining operation of the FHA insurance programs for the foreseeable future. “ Updated and current technology should be able to identify specific loans and generate aggregate reports on claims paid for property’s in assignment, those which were terminated, foreclosure expenses, and property management costs for REO properties.

Improved servicing

The prompt sale or payoff of a property with a terminated or foreclosed HECM loan will help ensure against avoidable losses and asset depreciation.

When FHA Commissioner Dana Wade called for the removal of the HECM from FHA’s fund NRMLA President Steve Irwin perhaps best expressed the unfinished business that warrants attention in his written remarks to Reverse Mortgage Daily, “I think that before there can be a thorough analysis of such a move, the Department should continue to work to improve the servicing performance of HECMs that have been assigned to HUD. Once the issues on the back end of the HECM lifecycle can be resolved, and the front-end changes that have been implemented over the past several years have been fully considered in the modeling of the program, we should see the fund restored to a positive net worth.”

Although not specifically addressed, one of the concerns by many industry stakeholders are unoccupied HECM properties falling into disrepair, and unauthorized parties occupying the property after the last borrower has died or moved away- both which impact the value of the property and increase the loan balance leading to a likely payout from the fund. Increased staffing and supervision of HUD-appointed servicers for HECMs in assignment would help improve performance and reduce occupancy fraud and property devaluation.

Regional Principal Limit Factors

Just as all real estate markets are local, home appreciation rates vary significantly by state, county and local neighborhoods. Outside of interest rates, the starting home value and principal limit factor or lending ratios has a large part in determining the likelihood of FHA paying out an insurance claim. FHA is not unaware of the regional variations in home values which has led them to call to abandon the present national lending limit in favor of county-by-county maximum claim amounts. However, those with moderately priced homes in poorer counties stand to be disproportionately impacted. Those of you who originated HECM prior to the national lending limit can recall lending caps hundreds of thousands of dollars below the Maximum Claim Amount benefiting homeowners in larger metros. Instead of county lending limits averaging all home sales, PLFs would be assigned to areas based on historical appreciation. Those areas with a record of little or no appreciation would have lower PLFs to reduce the risk of the loan payoff exceeding the home’s value at loan termination.

Leave liabilities

Lastly, any move of the HECM to another fund should leave any existing liabilities from prior loans behind. Otherwise, the program would face the herculean task of digging out from projected valuations which have not yet been fully realized in paid claims.

Change is endemic to the federally-insured reverse mortgage. Today the opportunity to address decades-old dilemmas is before us. What path will be taken remains to be seen.

Additional resources cited:

RMD column: Should FHA Exclude Reverse Mortgages from the MMI Fund?

HECMWorld column: The Tip of the Iceberg: HECM Occupancy Abuses