![]()

Older workers face ‘involuntary retirement’.

Are we reaching these homeowners?

- In January 2020 the unemployment rate for those 55 and older was 2.6% [MarketWatch]

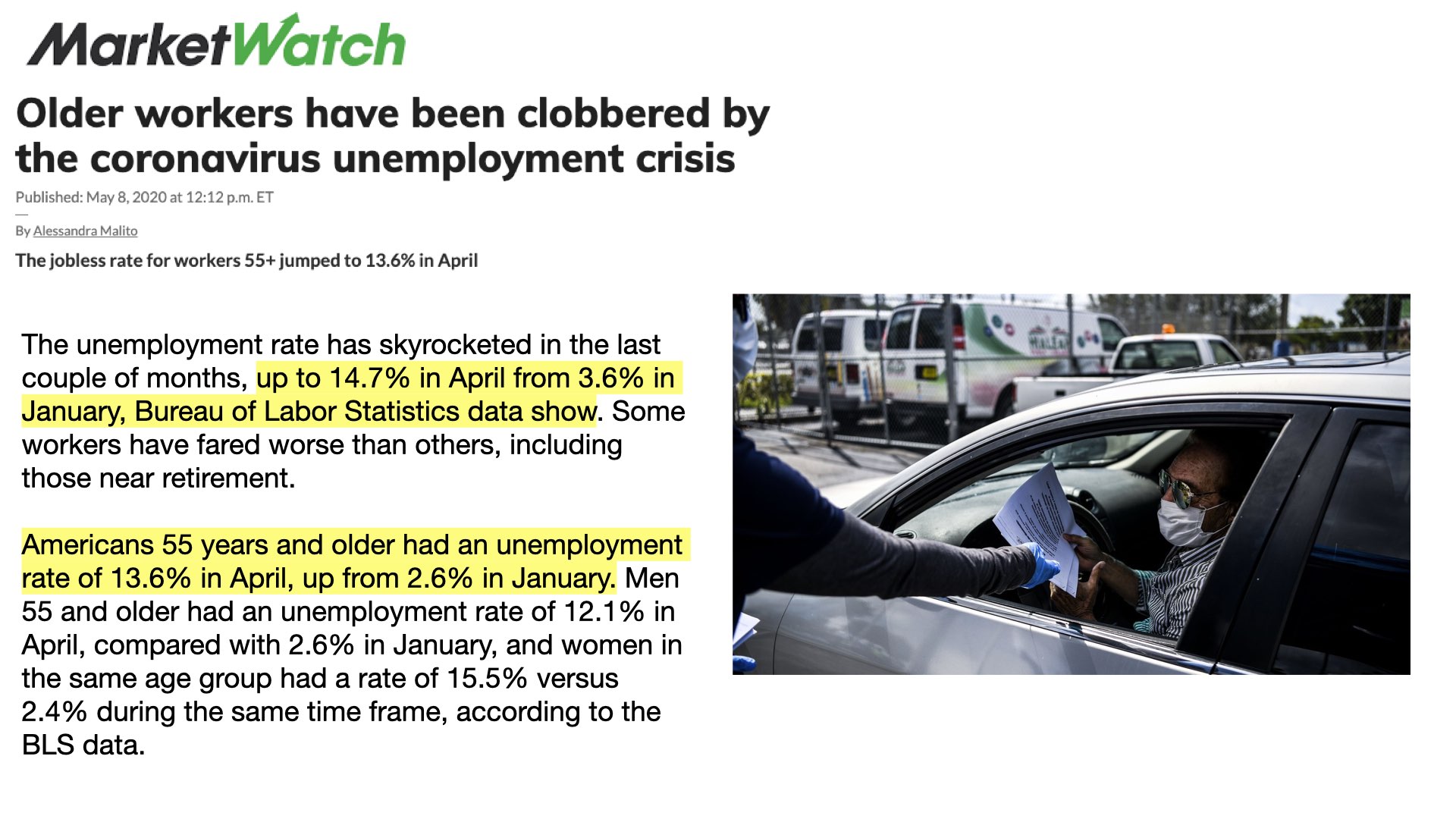

- By April 2020 the unemployment rate spiked to 13.6% for those 55 and older [MarketWatch]

- After the last recession (2008) those between the ages of 51-60 waited for an average of 9 months before finding new employment while those 25-34 were working within 6 months. [Urban Institute]

Many older Americans are still working, or at least recently were. Either way, they must meet their daily living expenses. This demographic while not completely forgotten is rarely mentioned. Even on this show I typically say a reverse mortgage may help those in their non-working years or retirees. However, a recent column caught my attention.

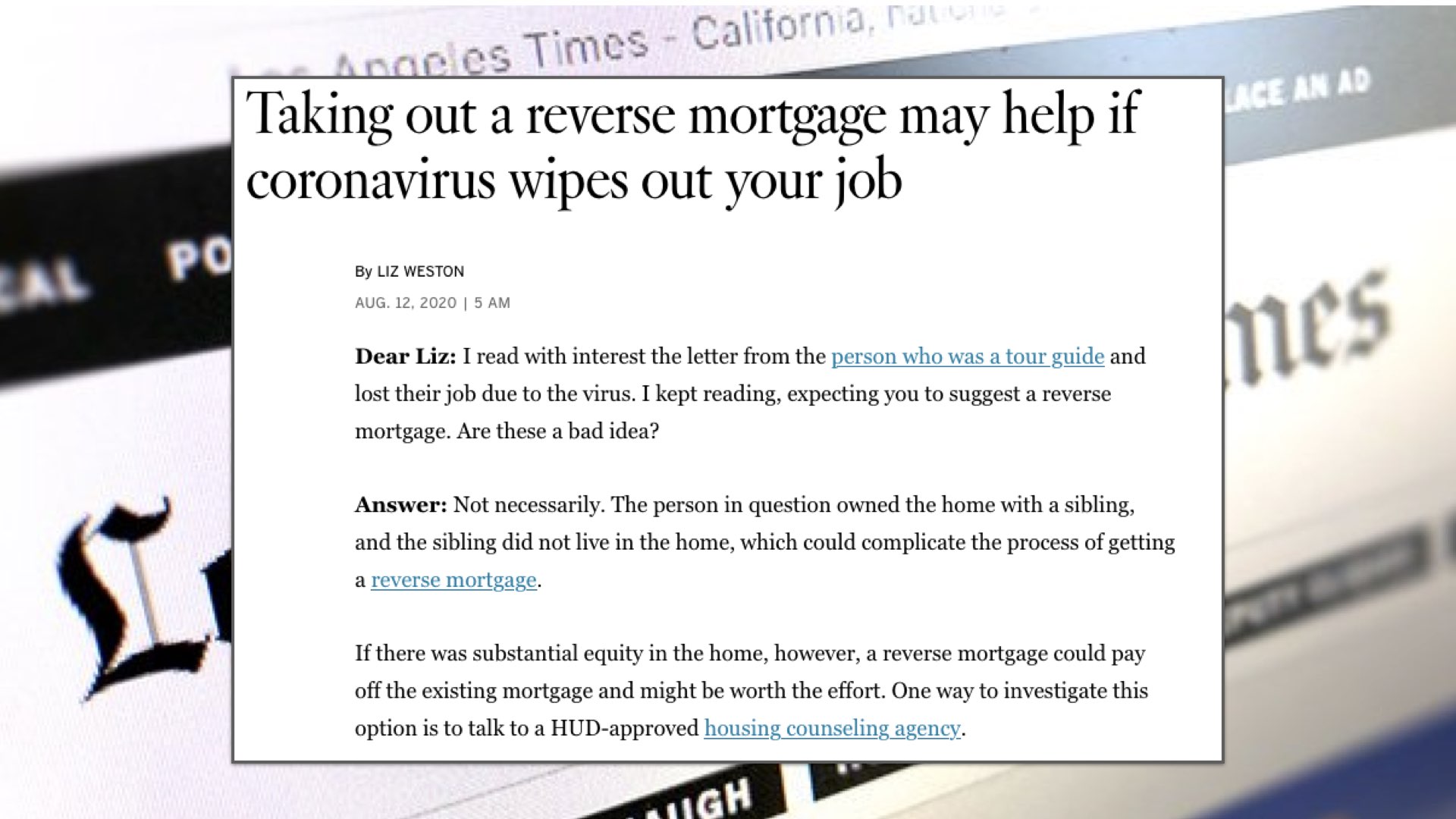

“Dear Liz”, writes one reader to LA Times columnist Liz Weston, “I read with interest the letter from the person who was a tour guide and lost their job due to the virus. I kept reading, expecting you to suggest a reverse mortgage. Are these a bad idea?”. Weston replies, “not necessarily” and then goes on to explain if there’s sufficient equity in the home a reverse mortgage could pay off the existing mortgage and “might be worth the effort”. In May MarketWatch noted Americans 55 and older have been clobbered by the coronavirus’ economic fallout…

[read more]In January of this year, MarketWatch notes the unemployment rate for those 55 and older was 2.6%. By April that unemployment number jumped to 13.6%. While our youngest workers have a higher rate of unemployment, older unemployed workers face unique challenges. The Urban Institute found that after the last recession of 2008 those between the ages of 51-60 waited an average of 9 months to find a new job while those 25-34 were working again within 6 months. Age discrimination is easier to recognize on the job but is much more subtle during the hiring process. All which leads us to the undeniable fact that millions of older homeowners are facing a forced retirement and financial crisis.

The good is many may find their solution literally right above their heads and in the walls that surround them. Where unemployment benefits and a loss of income create a cashflow crisis reverse mortgages will increasingly become the logical solution.

So let’s step back for a moment and consider our marketing. What is our message? Are we using the term retiree repeatedly? Do our mailers, emails, and online ads ASSUME that the homeowner is retired? It may be time to tweak our approach to appeal to the unemployed worker over the age of 62 who owns a home. So, practically how could YOU reach this target audience? One possible approach is to host workshops on the subject of ‘INVOLUNTARY RETIREMENT’ -for older workers who were laid off. These sessions could include short presentations from key senior service providers or experts and of course feature how homeowners may leverage their home to replace lost income with a reverse mortgage’s loan proceeds. CPAs and financial advisors may want to begin to inquire about their client’s employment status which may have changed as a result of the pandemic. Another tactic is to reach out to your local television and radio stations to pitch an interview on the impacts of unemployment for older residents and realistic solutions.

On August 6th PlanSponsor-dot-com wrote that The New School’s Retirement Equity Lab expects another 1.1 million older workers will leave the labor force in the next three months. The need to fund retirement is ever-present but the more immediate and pressing challenge of INVOLUNTARY RETIREMENT or unemployment of older Americans should spur our specific and strategic efforts. In summary, the solution remains the same while our approach should evolve to adapt to the specific pitfalls our present economy presents.

[/read]

Listen to this episode here: