How many borrowers in 2020 may benefit?

While HUD’s announcement of the increase of the lending limit for federally-insured reverse mortgages is a  positive development, it will likely only benefit a minority of future HECM borrowers in 2020.

positive development, it will likely only benefit a minority of future HECM borrowers in 2020.

HUD’s 2019 annual report to Congress reveals that the average maximum claim amount (MCA) for HECMs endorsed in the fiscal year 2019 is $347,275- a number which has increased substantially from $262,000 in 2009.

So just how many future borrowers could be aided from HUD effectively raising the ceiling of the home value that can be considered when determining loan proceeds? To answer that question we first needed to ascertain how many HECMs exceeded 2019’s MCA. A daunting task, that is until we reached out to John Lunde, President of Reverse Market Insight.

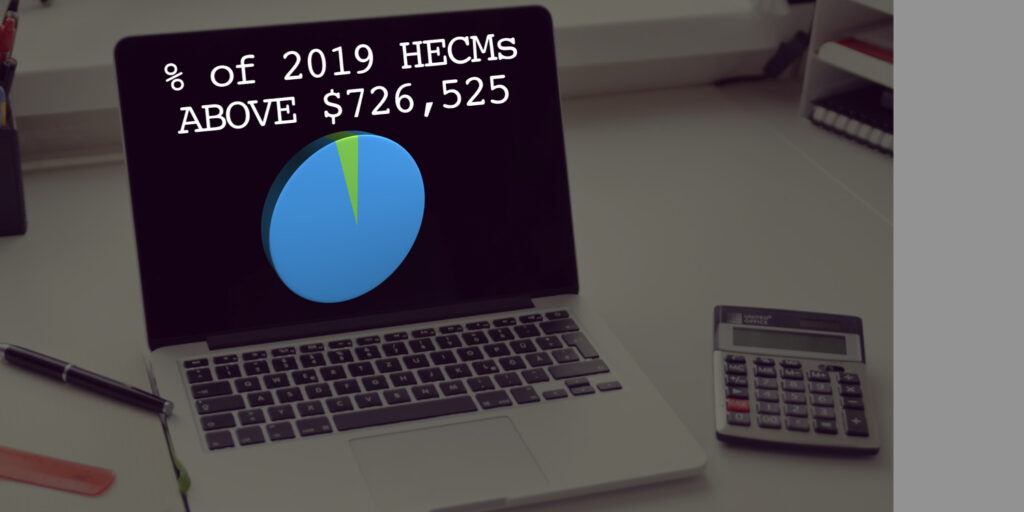

A total of 1,272 HECMs endorsed in the fiscal year 2019 were appraised at or above the lending limit of $726,525 according to RMI which tracks our industry’s key metrics.

[Learn more how RMI can help you understand your local market]

That’s 4% of the 31,274 loans endorsed in FY 2019 appraised at or above $726,525. One could conclude a similar percentage of borrowers in 2020 may stand to benefit- some up to $19,654 more in their gross principal limit (available loan proceeds before closing costs, insurance, and payoff of liens).

That’s 4% of the 31,274 loans endorsed in FY 2019 appraised at or above $726,525. One could conclude a similar percentage of borrowers in 2020 may stand to benefit- some up to $19,654 more in their gross principal limit (available loan proceeds before closing costs, insurance, and payoff of liens).

If there is cause for widespread optimism in 2020 it is this: Congress has not approved HUD’s proposal to eliminate the national lending limit and return back to county or regional lending limits. A return to regional MCAs would severely impact those with moderately-priced homes who have the misfortune to live in a county with lower home values.

All things considered, there is a reason to be thankful. Originators in higher-valued markets can check their CRM/database for those who were short to close and may be able to qualify in 2020. Those in other markets can exhale seeing that the national lending limit remains in place presently.

2 Comments

Good analysis: “4% of the 31,274 loans endorsed in FY 2019 appraised at or above $726,525.” All things being equal, those borrowers would surely receive higher principal limits if originated in 2020. However, that doesn’t tell us how many $1mm homeowners will be enticed by the new $765,600 limit in 2020. Consider that if the HECM limit doubled to $1.5mm, the 4% statistic would still hold true, but there would be a heck of a lot more HECMs next year. My guess is that $765,600 is significant enough to put some upward pressure on HECM volume, but proprietary innovation may put a lid on it.

Well said, Dan. I can always count on you for unique insights. I agree in hoping for a stronger pull-through of higher-valued homes beyond 4%.