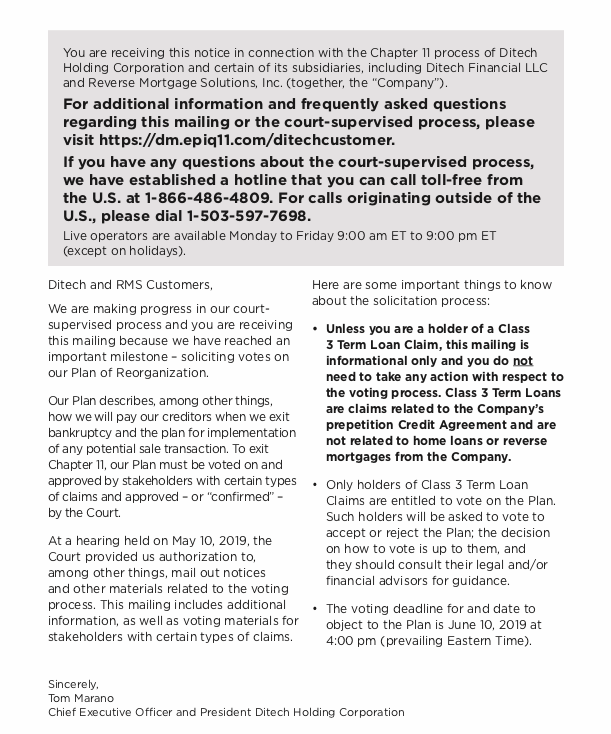

HECM borrowers with loans serviced by RMS have questions after receiving bankruptcy notices from Ditech

The financial woes of Ditech have been documented in recent months. The parent company of RMS (Reverse Mortgage Solutions) is sending out required notices of Ditech’s bankruptcy proceedings which have triggered concerns for many borrowers.

We received the following contribution from Tim Linger HECM Senior Home Financing which spells out what borrowers with loans serviced by RMS need to know.

Submitted by Tim Linger

Borrowers with HECM loans serviced by Reverse Mortgage Solutions (RMS) are receiving  letters indicating the bankruptcy filing of Ditech, a parent company of RMS. As you can imagine, borrowers are concerned.

letters indicating the bankruptcy filing of Ditech, a parent company of RMS. As you can imagine, borrowers are concerned.

HECM loan servicing is an important part of the overall HECM process. Reverse mortgage loans stay in this final stage of servicing for the majority of their existence. The other loan stages such as origination, processing, underwriting, closing, and funding, are rather brief in comparison to the servicing period.

The originating broker or initial lender may or may not be the servicer of the HECM loan. In all likelihood, the loan’s servicing rights may be transferred between servicers during the life of the loan and perhaps, even assigned to HUD’s contract servicer before the loan is ultimately terminated.

The servicing company is important to the borrower(s) because their servicer is the central point of contact when questions arise about their loan.

What happens when the servicer ceases operations or no longer services the HECM per the original loan contract? The answer is, per HUD’s guarantee, even though the loan servicer may change, the terms of the HECM remain the same.

You see, the rules of reverse mortgages are determined by the written promises made by the lender to the borrower(s) in the legal closing documents (Note, Deed of Trust and Security Agreement) that the borrower(s) signed at the closing of the HECM.

Regardless of who services the HECM, the borrower(s) can only require those specific items agreed upon in the initial legal documents signed at closing. FHA insures the HECM and therefore, guarantees that no matter may happen to the Servicer, the borrower(s) continues to have a safe and valid contract.

The two common questions from Borrower(s) are: ‘is my HECM safe and, ‘what do I need to do?

First, don’t panic. The purpose of FHA’s Mortgage Insurance Premium (MIP) should give all Borrower(s) full faith that the full faith of the federal government (FHA / HUD), is backing the HECM program and the terms of the loan. The servicer is ultimately communicating what FHA has promised and their guarantees are solid – as solid as the federal government. Yes, the HECM is safe.

Second; What do I need to do? Nothing, unless the borrower(s) feel they have a claim to file. Rest assured that FHA is on the case! HUD guarantees that the loan will be serviced properly, or that the servicing rights would be transferred to another servicing company. Monthly statements, loan proceeds, lines of credit, additional fees, and all terms of the contract will not be affected or changed by any entity, including RMS or it’s parent company’s (Ditech) bankruptcy filing. Sit tight and relax, everything is going to be alright.

Written by Tim Linger, CHS, CRMP, CSA, President of the HECM Association

Tim Linger is a Certified HECM Specialist, Certified Reverse Mortgage Professional, Certified Senior Advisor, and the President of the HECM Association – a 501(c)3 non-profit trade association. Tim has nearly 20 years exclusively in the reverse mortgage arena and prides himself on knowing the HECM thoroughly. Tim is based in Orlando Florida and is the owner of HECM Senior Home Financing Inc. His brokerage focuses on the HECM for Home Purchase. Tim can be reached at TimLinger@HECMsenior.com or direct at 321-356-9229

12 Comments

I got a call just yesterday from a borrower and had to Google the case as I had not yet read about it. I was able to find it quickly and assure him there was nothing he needed to do. But I can see how many would be concerned when first opening that letter.

Melinda:

I am glad I could help.

It is sad that a once great company (RMS) could come down to this.

they are a horrible Servicer now (many problems and no responses from CS)

I hope that HUD takes over their Servicing rights

Thx

Tim

Tim,

Great Explanation.

Thanks Dick.

Are you still originating HECMs?

Email me at TimLinger@HECMsenior.com and let’s catch up!

Thx

Tim Linger

321-356-9229

The explanation is interesting but adds more questions as well as answers some basic ones.

For example, what does the following sentence mean? “Regardless of who services the HECM, the borrower(s) can only require those specific items agreed upon in the initial legal documents signed at closing.” What exactly are “borrower(s)” requiring in relation to the RMS bankruptcy.

What does the following mean? “The purpose of FHA’s Mortgage Insurance Premium (MIP) should give all Borrower(s) full faith that the full faith of the federal government (FHA / HUD), is backing the HECM program….” MIP are premiums on an insurance contract that the borrower does not sign. The payment is not required to be paid by the borrower. It is only required to be paid by the lender or its servicer but it is a fully reimbursable item from the borrower. Right now I am negotiating the IMIP to be paid in full by the lender and absolutely nothing by the borrower. The borrower is but an incidental and indirect beneficiary (but an important one) to the insurance contract. The implication SEEMS to be that MIP makes the HECM nonrecourse which is utter nonsense. It is that same contract that the author relies upon to determine the terms of the loan that makes a HECM nonrecourse — JUST LIKE every other reverse mortgage.

The next statements are incorrect: “What happens when the servicer ceases operations or no longer services the HECM per the original loan contract? The answer is, per HUD’s guarantee, even though the loan servicer may change, the terms of the HECM remain the same.” It is the lender that guarantees there will be a servicer. In some cases, HUD may be the guarantor but that is, generally, only when HUD has asserted its rights in the contingent loan docs that show HUD as the lender.

This is what happens when originators try to explain concepts that are legal in nature. Only in RARE, situations is there sufficient legal knowledge to determine whose responsibilities are whom’s and whose rights are whom’s. It is clear that the explanation above lacks accuracy.

Thanks for your feedback Critic…

Obviously there are some typos and perhaps some poorly worded sentences (by bad). Perhaps the Editor can correct them?

I do feel that most readers can & will interpret these errors and understand their meaning of each sentence.

As far as your MIP concern and, Lender/HUDs guarantees, etc, etc. We are limited in space (# of words) for this article. To explain everything in legal-speak would be a booklet. To explain everything with details would complicate these simple answers for our readers. The point to this article is to give peace of mind to the MLOs and to their clients. I am not saying you are wrong Critic.

Thx

Tim Linger

This consumer needs an answer to who is actually in charge of finding another servicer ? At what point would it be deemed to have to find another servicer? Would a new servicer offer terms to negotiate or just simply take over as the servicer with nothing changed? Do you really think we as reverse mortage consumers can have trust in HUD who is lead by an inept leader? Thank you, Rosalind

The vast majority of the staff at HUD is very competent. Even (as you say) their leader is not. One person (i.e. the leader) doesn’t make all the decisions. So yes, your loan’s viability and the stability of your HECM (reverse mortgage) is safe in the hands of HUD. When/if HUD decides that a new Servicer is needed, HUD has the sole discretion of making that servicing transfer decision (not the consumer). The new servicer must provide the same terms -, nothing will change and nothing to negotiate. Thanks for your comments and questions.

Mr. Linger,

What if the servicer is a subservicer? Then the subservicer can be replaced by the servicer and not necessarily by HUD. Servicing rights can be sold by the servicer to another servicer as well.

Do not think that one or many corrections by HUD means every mortgagor now has a correct balance due , line of credit balance, or other details. Those corrections show that mortgagors need to pay even more attention to their monthly mortgage statements. Unfortunately, many IRS Forms 1096 have either been neglected to be sent out or sent with incorrect information.

Mortgagors should never be passive when it comes to accounting for their own mortgages.

What do MLOs have to do with servicing? Like any other person, MLOs have no special or unique rights to get mortgagor information from the servicer WITHOUT the permission of the mortgagor. MLOs are NOT agents for the servicer nor are they attorneys. Even if a MLO is an attorney acting as a MLO, mortgagors cannot rely on the attorney/MLO to provide legal services to the mortgagor as well unless there is a separate

agreement to that effect. If mortgagors need to know about that their legal rights with a servicer, they should seek the advice of an attorney who is competent in such matters and did not act as the MLO as to the mortgage under question.

Mortgagors should also be no less than reactive in reviewing their monthly mortgage statements. They should immediately question the serviver about everything they do not understand or that is blantantly wrong. Servicers MAKE ERRORS. If a mortgagor finds the servicer to be less than cooperative in getting their questions answered they should report the incidence(s) to HUD and the CFPB

No mortgagor who has his/her mortgage serviced by RMS should relax or be passive about their reverse mortgage, period. It is by its nature a GROWING debt.

Who decides when a servicer will be replaced? At what point would RMS be replaced? Do you personally expect us to have high confidence in the leader of Hud, who is totally inept?

Tim,

You are a nice guy but stop acting as an advocate for RMS. You are playing with fire. Who knows what mortgagors have been HARMED by RMS? I know I don’t.

Why is this notice being posted? Every originator has the right to present myths at any time but why do we as an industry so easily adopt them?

Rather than trying to sooth the worries of borrowers when it comes to servicers, we should be looking into them. It is very unlikely that anyone with the competence to review the details of the borrower’s account at the servicer has done so. For example, even before declaration of bankruptcy, RMS paid a costly penalty to HUD due to its double charging of fees.

Do readers really think that all bad accounting practices, errors, potential wrongdoing by RMS has been discovered or disclosed? Unfortunately, most borrowers either do not verify their monthly statements or do not have the skills to do so. We need to care for our borrowers, not write carelessly in an attempt to make feel as if servicers are accurate and are looking out for borrowers’ best interest.

If we do not have the time, interest, or space to say things the way they are, then we should be directing borrowers to practitioners who can help them.

To be clear, borrowers should not be relaxed or have peace of mind, until a competent party has reviewed their mortgage statements for accuracy including detection of inappropriate charges. Just because some fines, penalties, court awards, and other findings have been made, that should not give ANY borrower confidence that everything is OK with their reverse mortgage account accurately reflects their balance due or available line of credit. Servicers make errors and too many times do not review their work and thus never even attempt to correct them.