EPISODE #732 Why Ramsey Solutions’ housing forecast may not age well

“Right now is the best time to buy a house in the next five years. And here’s why: prices are not gonna go down”, says Ramsey Solutions, the company founded by the financial celebrity and well-known commentator Dave Ramsey. Is he right?

Other Stories:

Senior housing wealth up 4.91% in the first quarter of 2022

EPISODE #730 Should I sell and rent or get a reverse mortgage?

One 82-year-old woman writes a Money Sense columnist saying her savings are draining fast and she wants to know if she should move & rent or consider a reverse mortgage.

Other Stories:

Social Security Recipients Could Get a Massive 11% Raise Next Year (Money.com)

Equity-rich homeowners find themselves squeezed between inflation and a volatile stock market

We should never forget that today’s economy isn’t just a hardship for retirees, for many it’s an outright nightmare. Older Americans are seeing their purchasing power evaporate as they ratchet up retirement withdrawals in the effort to stay afloat. Older renters who don’t have a nest egg of home equity built up are feeling the worst effects of inflation.

[read more]

The Pensacola, Florida station WEAR-TV reports one 64-year-old retiree, Ruby Gilbert, is going back to work and is looking for a job after the rent on her Lantana, Florida apartment was increased from $1,450 per month to nearly $2,000.

Inflation has another insidious side-effect; reduced retirement savings. Many pre-retirees have reduced or halted their automatic retirement savings investments finding life is getting just too expensive to save for tomorrow. The impacts of depressed savings will be felt in the next five to ten years.

All is not lost, however. In fact, one group of retirees may unwittingly be sitting on top of a potential solution to their inflation-driven cash flow woes. Homeowners. Some of the same policies that led to a surge in domestic inflation also inflated home values. And that’s good news for seniors on a fixed income who feel the brunt of inflation with housing, food, energy, and gasoline accounting for 75% of a typical senior’s budget. The challenge is the growth in home values that may help older homeowners has also damaged the overall housing market.

The run-up in home values has become so absurd homebuyers are finally deciding to stand on the sidelines.That’s not surprising considering the recent surge in 30-year fixed-rate mortgage rates coupled with peak home prices has made homeownership unaffordable for millions. Once again the housing market would have been relatively undamaged by a sudden rise in home mortgage rates if home appreciation grew at typical rates of 3%-4% a year. However, the Fed’s policies stoked another irrational white-hot housing market.

That leaves retirees facing uncertainty. For example, the S&P 500 index closed down 18% year to date while Moody’s Analytics data suggests the average home value is inflated by 24% with values outpacing income growth. In such circumstances, older homeowners are being squeezed on all sides with a declining retirement portfolio, inflation, and hundreds of thousands of dollars in equity that could begin to erode this year. Right now it’s too early to tell if we’ll have a housing market crash or a correction but mark my words, we will have one or the other. Housing prices cannot remain at these inflated values without the support of underlying economic fundamentals. Home sales have fallen four months in a row while the number of new home listings is surging across several key U.S. metros. And there’s a dirty little secret hiding in plain sight. The U.S. Census Bureau reports that 13.4 million Americans are either currently in default on their home payments for a mortgage or rent. Nearly 5 million of these households will be foreclosed on or evicted in the next two to three months. While these displacements are genuinely tragic they will substantially increase housing inventory putting pressure on home prices and rental rates.

Ironically loan delinquency rates are down 1.93% month-to-month and 42% less than they were one year ago according to Black Knight data. If the U.S. enters a recession, which seems a likely outcome, expect to see foreclosure start and filings surge. All things considered, older homeowners with considerable equity stand best-prepared to cope with the increasing cost of living. The question is are they aware of their options?

EPISODE #728 The 2 forces are slowing the housing market’s return to normal

The ongoing housing supply shortage is exacerbated as people stay in their homes longer than in years past. Economists have identified a pair of trends combining to slow housing market normalization.

Other Stories:

Reverse Market Insight’s Market Minute

A leading indicator? Three lenders revise private reverse mortgage products

The mortgage meltdown.

Are reverse mortgages the recession-proof solution?

The pieces are now falling into place. Consumer spending has dropped considerably. Large ticket items and even housing could see deflation. Inflation is crushing consumers who are now cutting back on discretionary spending. Last week the nation’s two largest retailers Walmart and Target reported massive drops in profits. Target alone shed 25% of its stock value last week after reporting a stunning 52% drop in profits. CNN Business reports Target was also forced to write down the value of excess inventory that’s just sitting in warehouses. In other words, consumers are on strike only buying necessities.

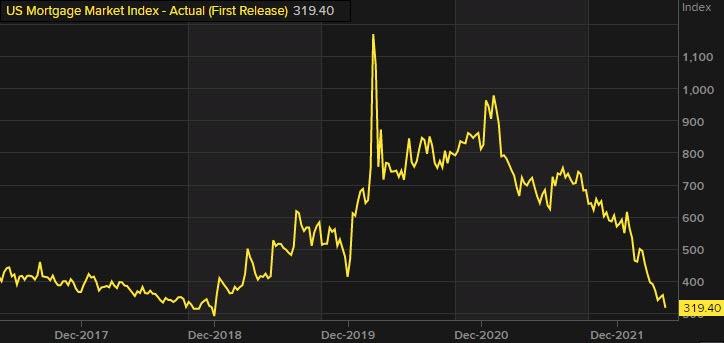

Traditional mortgage lending is feeling the full force of economic forces that have returned to roost after a decades-long absence; inflation and rising interest rates.

On the supply side…

[read more]

the National Association of Homebuilders released a report that homebuyer traffic for new homes is down 29% year-over-year from May 2021. In a statement, the association said, “In a sign that the housing market is now slowing, builder confidence took a steep drop in May as growing affordability challenges in the form of rapidly rising interest rates, double-digit price increases for material costs, and ongoing home price appreciation are taking a toll on buyer demand.”

The finance side of the housing market is feeling the full force of this economic storm. The average 30-year fixed mortgage rate began at 3.66% in February and is now floating around 5.45%. Consequently, purchase and refinance applications have tumbled. Mortgage News Daily reports both suffered double-digit hits with its Market Composite Index that measures application volume dropping 11% from the previous week. Year-to-year application volumes are down 15%. Refinance volumes have fallen off a cliff. Today home refinances are down 76% from May of last year.

The issue is not merely interest rates. Case in point, in November 2018 the average 30-year fixed-rate loan was nearly five percent or just one-half point less than today’s average rate. The rub is both the massive inflation of home values and consumer goods. The median home price in November 2018 was $322,800; today it’s $428.700. The Consumer Price Index (a measure of the inflation of consumer goods) was only 2.2% in November 2018. Today the annually-adjusted inflation rate is estimated to be 8.5% It’s natural that higher mortgage payments coupled with the rapidly-increasing price of consumer goods is pushing many out of the housing market and forcing others to discard any hopes of a cash-out refinance or HELOC.

As a result, many mortgage lenders are now eying reverse mortgages, and who could blame them? Unlike younger homeowners who have little or no equity, older homeowners are sitting on trillions of dollars of accumulated equity- many who would qualify for a reverse mortgage, even at today’s interest rates.

Anecdotal reports already indicate today’s changing market is pushing many who’ve previously considered a reverse mortgage off the fence. Traditional mortgage lenders without a reverse mortgage division will find the move into reverse not only logistically challenging but culturally foreign to most of their originators. However, those lenders who have already bifurcated their business into traditional and reverse can more easily pivot prioritizing their investment and energies toward reverse lending. Wholesale mortgage brokers will be shopping for turn-key reverse mortgage business models.

One thing is certain. The historical increase in reverse mortgage loan activity corresponds with the number of lenders actively originating the loan. Does this mean we will see the return of one or two large retail banks? It’s too early to tell. However, with necessity being the mother of innovation we can expect to see more small to midsize banks and mortgage lenders move to reverse. In the end, that’s a good thing.

The Math proves it.

The time to use an inflated asset to offset inflation is ending

If there’s one word that comes to mind when describing home prices today it’s inflated. Today’s inflated home values are primarily a product of two things: years of cheap money (low interest rates), and a long-term shortage of housing inventory.

Reflecting on the current state of the housing market many may say, “something has to give”, meaning this cannot possibly last forever. They’re right.

What does ‘reverting to the mean’ look like for the U.S. housing market?

What’s likely to happen is a reversion to the mean.

Not a nasty person or a ‘mean’ housing market, but a return to the historic norm. Let’s take home appreciation. Just like gravity eventually pulls an object back to earth, economic forces eventually exert enough resistance to pull back home appreciation rates back to their historical mean.

The reversion of home price appreciation is the natural result of a highly speculative, abnormal, and highly-inflated market. It’s also extremely painful for those who may have lost the opportunity to restructure their debt while tapping into some of their home’s value.

The impact of repeated interest rate hikes would generally be offset if home values miraculously continued to appreciate by 15-20% a year. The fact is such daydreams never materialize; especially not when potential homebuyers have fewer dollars to invest in a home thanks to historically-high inflation that shrinks their dollar each day.

Despite a historically-established record of housing booms, busts, or deflations, many homeowners choose instead to believe the myth that home values will never fall. Of course, they will and do. The question is what happens to those who don’t secure some of their home’s value only to see it drop by ten, fifteen, or twenty percent?

For those who are not cash strapped despite the spike in the cost of living the answer is ‘very little’. However, for many, the regret and anguish will feel as real as the bricks in their home. They missed the opportunity to leverage an inflated asset (their home) to offset the inflation of the costs of goods and services during retirement. That’s when a reversion to the mean in home values can feel quite nasty.